Disclosure:

Remember that this material is intended to provide you with helpful information and is not to be relied upon to make decisions, nor is this material intended to be or construed as legal advice. You are encouraged to consult your legal counsel for advice on your specific business operations and responsibilities under applicable law. Trademarks used in this material are the property of their respective owners and no affiliation or endorsement is implied.

Tax season is upon us, and if you own rental real estate, then you may have a federal tax responsibility to report all rental income on your tax return. The IRS defines rental income as “any payment you receive for the use or occupation of property”, and may include:

- Normal rent payments

- Advance rent payments

- Security deposits

- Tenant payment for canceling a lease

- Tenant-paid expenses

- Property or services received, instead of money, as rent

Taxes can be intimidating for both first-time and even seasoned landlords—especially during the events of the last few years. Afterall, one wrong tax move and you could see your rental business get sucked down the drain.

With eviction moratoriums ending, rents rising to record levels, and other financial uncertainties leftover from the pandemic, it’s essential to find ways to save on your taxes and take advantage of deductions.

In addition to a sparkling tax return, you can maximize rental income by placing spotless tenants from the start. Before signing a lease or handing over the keys, conduct thorough renter background screening with a reputable service like SmartMove.

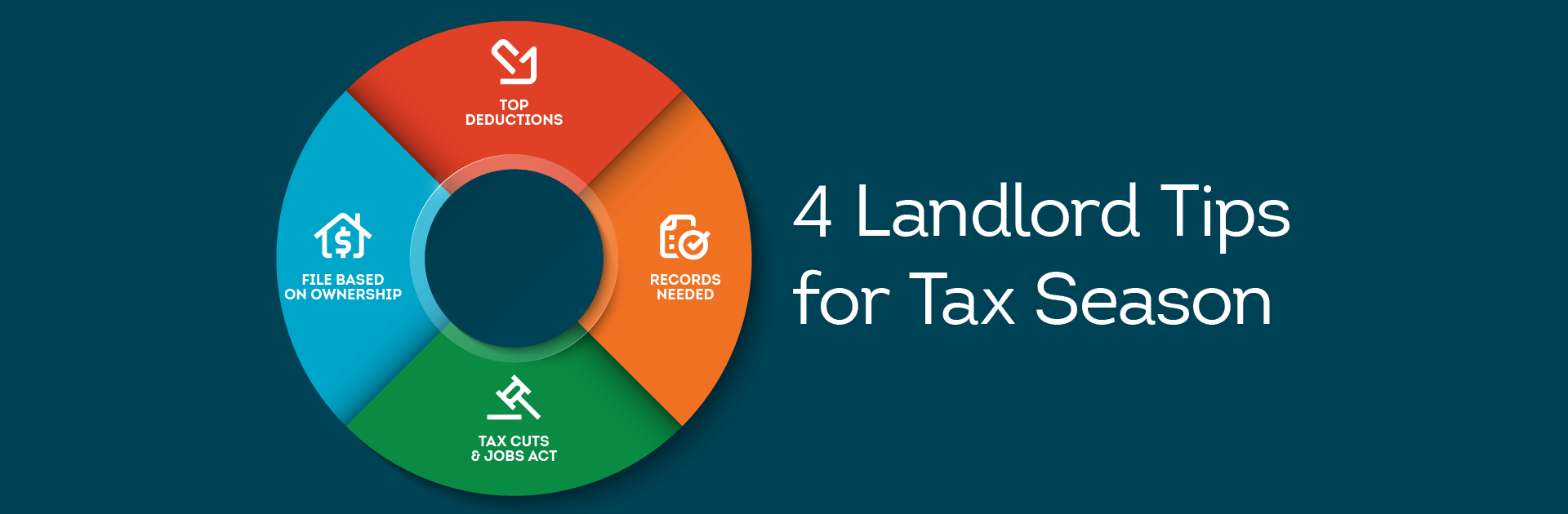

To help you make it through this 2022 tax season and get the most out of your tax return, we’ve rounded up some of the best articles featuring tax tips for landlords.

These articles cover:

- Tax Deductions: Learn what you can deduct to increase your tax savings.

- COVID Resources: Discover key resources for navigating landlord responsibilities in the wake of the global pandemic.

- Record-keeping: Determine which documents you need on-hand when filing your taxes.

- Tax Cuts and Jobs Act: Read how new tax laws have shifted the tax landscape for landlords.

- Filing Taxes: Discover how to file your taxes based on your rental business setup.

These fresh tax tips for landlords, could help maximize your refund and keep more of your hard-earned money.

1. Top Tax Deductions for Landlords

Why pay more taxes on your rental income than required? Landlords can claim a variety of IRS deductions. NOLO’s article “Top Ten Tax Deductions for Landlords” covers essentials to consider when filing.

These deductions include:

- Depreciation for Rental Real-estate Property

You may be able to recoup some of the cost of your real estate investment through depreciation. Landlords are allowed to deduct a portion of the total cost of their property over several years. Learn more about deducting long-term assets here.

- Insurance

Did you know that you can deduct the premiums paid for many types of insurance you’ve purchased for your rental property? From flood insurance to landlord liability insurance, landlords generally are allowed to deduct some of the costs of insurance coverage.

- Repairs

Damages—whether caused by you or your tenant—are unavoidable. Fortunately, the costs of rental property repairs are often deductible for the year in which they are completed.

Do note that deductible repairs must be ordinary, necessary, and reasonable in amount. A few examples of applicable repairs include:

- Repainting your rental property

- Replacing broken windows

- Repairing gutters

These are just a few of the deductions you can claim for your rental business.

2. COVID Resources

It’s been another tumultuous year for landlords and tenants alike. Over the last few years, property owners shifted some landlord practices in the age of social distancing. From transitioning to virtual property showings to wading through moratorium regulations, there’s been plenty to keep track of.

With some return to normalcy hopefully in sight, many rental practices are returning to pre-pandemic standards. However, rental prices, turnover, and evictions remain unpredictable.

In fact, The Harvard Center for Housing Studies reports small, independent landlords received only about 50% of expected rental income during the pandemic.

The last COVID-19 relief package in 2021 provided $25 billion for rental assistance, allowing landlords to apply for funds on behalf of their tenants. Though direct payments seem to be behind us, there are still several resources that can help with your tax return.

Benefits.gov provides a list of helpful resources for landlords in the wake of COVID-19. The page includes webinars, editorials, forms, and news sources regarding hurdles faced in 2021 and 2022.

3. Records Landlords Need During Tax Season

As a landlord, it’s important to keep accurate records—especially if you plan to claim any of the deductions discussed above.

Maintaining organized landlord records can help ease the stress of tax season. If your rental documents are tidy, you can easily find receipts, track deductible expenses, and prepare your tax returns. The Balance gives a great rundown on landlord record-keeping.

Keep the following records organized:

- All tenant leases or rental agreements, for all of your properties

- All legal documents, including any court appearances, fines, or inspection reports required for the property

- Any type of permit you have taken out on the property

- Any records that pertain to your business entity

- Insurance policies

- Loan documents

- Tax records from the past years

- Real estate investment papers, including property titles or deeds

Landlords also need to consider their short-term records. These are documents related to income or expenses from the given tax year.

These may include:

- Rental property advertising and listing costs

- Mortgage interest

- Rental business credit cards

- Legal or professional fees for lawyers, etc.

- Receipts for repairs

- Receipts for rent payments

- If applicable, receipts for utility costs

There’s plenty to keep track of, but it may be worth the effort. Having these important documents on-hand could help reduce stress and streamline your tax filing process. to learn more tips on landlord record-keeping.

4. What Landlords Should Know About the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA)implemented key changes, some of which affect rental property owners. Fortunately, many work in a landlord’s favor.

NOLO broke down some of the ways TCJA law affects landlords. Here are some of the most noteworthy changes:

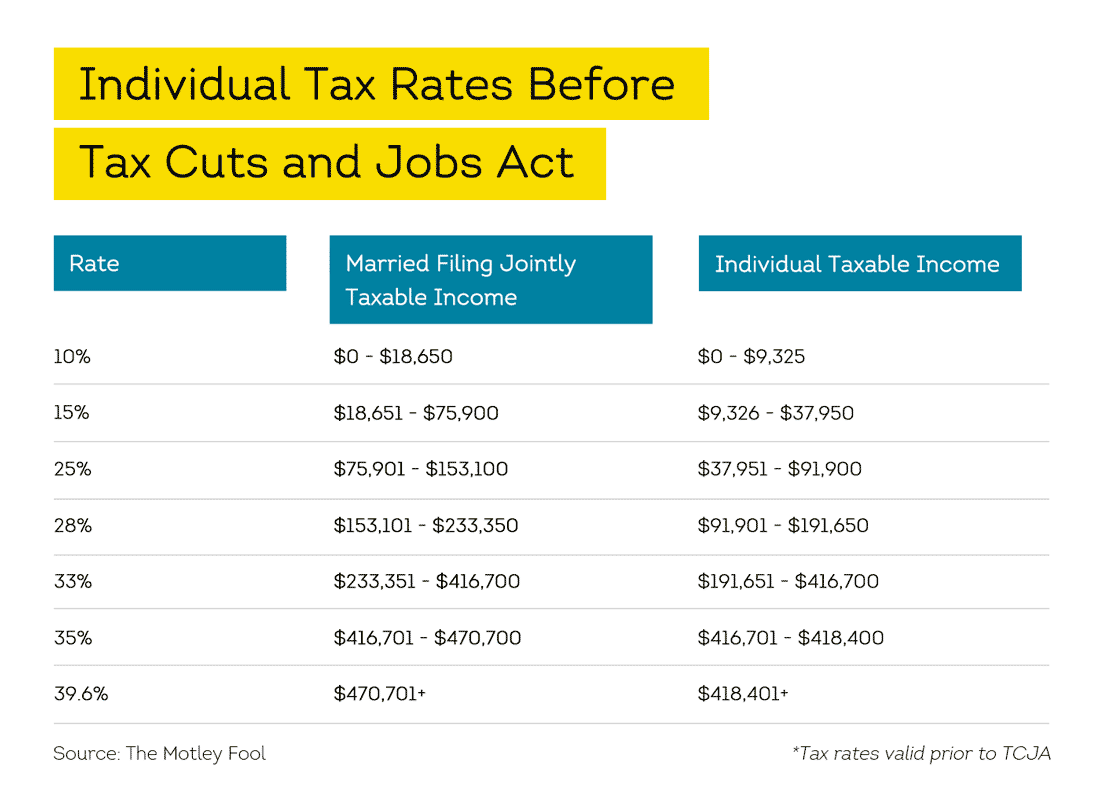

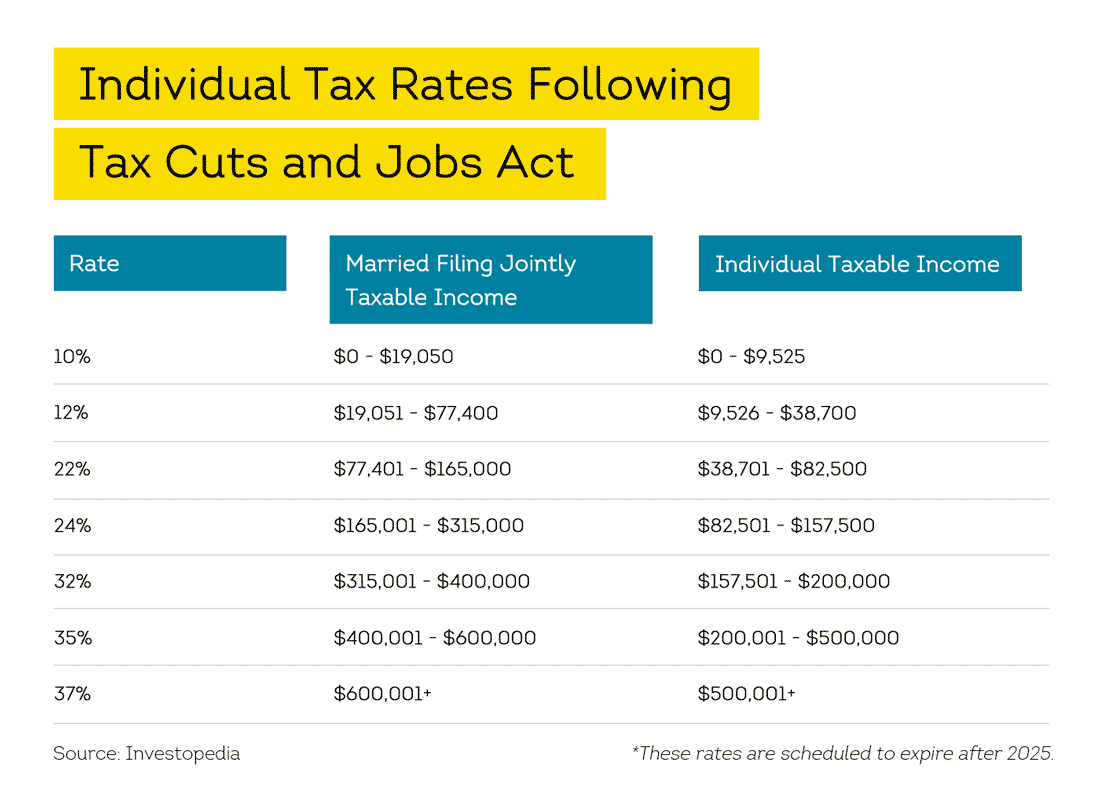

Change #1: Individual Tax Rates Are Lower

Many residential landlords are likely required to pay income tax on their rental profits at their individual tax rates. Before the Tax Cuts and Jobs Act, tax rates were as follows:

The TCJA reduces these individual rates until 2025, at which point they’ll expire. As of 2022, the individual tax rates are as follows:

Key Takeaway: Landlords might benefit from lower income tax rates.

Change #2: There’s a New Pass-Through Tax Deduction

Prior to TCJA, if you received net taxable income from one of the following pass-through business entities, that net income was taxed at your personal tax rates.

- Sole Proprietorship

- LLC treated as a Sole Proprietorship

- Partnership

- LLC treated as a Partnership

- S Corporation

Following TCJA, you might be able to take advantage of a new pass-through tax deduction, depending on your overall income level. If your rental activity qualifies as a business for tax purposes, you may be able to deduct up to 20% of your net rental income.

Key takeaway: Landlords that qualify for this deduction could see their tax burden eased.

Change #3: Section 179 Expensing Limit Has Increased

Section 179 allows rental business owners to deduct the cost of personal property used in their rental business, such as appliances, laundry equipment, or furniture.

TCJA expanded and increased this expensing level from $500,000 to $1,000,000. This is applicable for property purchased and placed into rental service from September 27, 2017 through December 31, 2022.

Key takeaway: Before TCJA, rental property owners couldn’t deduct the cost of personal property used in residential rental units. Following 2018, this restriction is no longer in effect.

To learn more about how TCJA might affect your taxes as a landlord this year.

How to File Your Taxes Based on Ownership Status

How you file your taxes depends on how you own your rental property. The article “Filing Your Taxes When You’re a Landlord” from NOLO explains how landlords should file their taxes based on rental property ownership:

Rental Property Owned Individually

- If you own the rental property by yourself: You can file IRS Schedule E, Supplemental Income and Loss, to report your rental income and expenses.

- If you own the rental property with a co-owner: Each co-owner should report his or her share of income and deductions from the rental property on his or her own tax return, using Schedule E. If you have a partner, each owner’s share should be based on ownership interest (which you can find listed on the property deed).

Rental Property Owned through a Business Entity

If you own your property through a business entity, then you should report your income and deductions from the property using IRS Form 8825, Rental Real Estate Income and Expenses of a Partnership or an S Corporation. Depending on the type of business entity, there are additional filing requirements.

Final Notes: Making the Most of this Tax Year

Filing taxes as a landlord doesn’t have to be a headache. Armed with the information above, and with the help of a tax professional, you can make the most of your tax returns.

As a landlord, you never want to lose out on money, whether it’s due to taxes, evictions, surprise tenant vacancy, or the non-payment of rent. allows you to gain access to detailed reports about your prospective tenant that can help you make a more informed decision about who occupies your rental property.

With SmartMove tenant screening reports, landlords are given the access to gain insight into an applicant’s credit history, Income Insights, ResidentScore, eviction and criminal history. Comprehensive reports are delivered in minutes so you can make a more confident decision quick.

Know your applicant.

Additional Disclosure:

For complete details of any product mentioned in this article, visit www.transunion.com. This site is governed by the TransUnion Rental Screening Privacy Policy Privacy Notice located at TransUnion Rental Screening Solutions, Inc. Privacy Notice | TransUnion.