Summary:

- ResidentScore® is a proprietary tenant scoring system from SmartMove that’s calculated based on real-world rental outcomes

- ResidentScore uses the familiar scoring range of 350 to 850 to help assess tenant eviction risk

- This exclusive score is included in every SmartMove screening package

Disclosure and Disclaimer

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied. Remember that this material is intended to provide you with helpful information and is not to be relied upon to make decisions. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation.

Many landlords are concerned about getting paid when they want to bring in a new tenant. These fears are exactly why many landlords conduct tenant screening through reputable companies, like SmartMove®.

You wouldn’t use a spoon to cut a steak. Sure, it might work eventually, but it’s just not the best tool for the job. Similarly, you may be using a sub-optimal tool for analyzing rental applicant finances––and may not even know it.

And, considering the time sink and high cost of eviction, it’s no wonder landlords are concerned. According to money site SmartAsset, an eviction can cost between $1,000 to more than $5,000, depending on a number of factors.

With this in mind, a new or seasoned landlord could find themselves in a costly and time-consuming situation if they haven’t done their due diligence during the tenant screening process.

In the past, landlords traditionally looked at their prospective tenant’s credit score to help them determine the level of risk before signing a lease. Even though traditional credit scores are generally designed to judge creditworthiness for financial products––such as home or car loans––they were one of the few options available for this kind of financial review.

But, then, SmartMove introduced ResidentScore®. Unlike traditional credit scores, ResidentScore was designed specifically for the rental market to help landlords assess potential eviction risk.

At first glance, both a traditional credit score and ResidentScore might appear to be similar. However, there are critical differences between the two that landlords should know about when screening a potential tenant.

This article covers how a traditional credit score works, the difference between a credit score and ResidentScore, and why landlords should consider using ResidentScore when making a leasing decision.

Traditional Credit Score vs. ResidentScore

Both a traditional credit score and SmartMove ResidentScore may help minimize risks when screening an applicant. However, ResidentScore is:

- Engineered for the rental marketplace, and

- Designed to help provide an assessment of potential eviction risk for your future rental property better than a traditional credit score.

With ResidentScore, you aren’t stuck basing your leasing decisions on the same algorithms that a bank would use. Instead, you get to use a score that specifically helps analyzes predictors of a bad rental outcome.

“A common misconception people have today about traditional credit scores is that they are all intended to predict the same type of credit quality and bad outcomes,” says Maitri Johnson, SVP Strategic Planning at TransUnion. “Banks and other financial institutions have been developing and maintaining industry-specific models for decades. There is no one score to predict all potential outcomes. Models exist to predict how likely you are to repay a student, mortgage, auto loans, and more. By using a model specifically intended to help predict rental industry outcomes, you may be better positioned to potentially identify good tenants than using a traditional credit score.”

To understand how ResidentScore can more effectively help predict eviction risk than a traditional credit score, the next section examines how traditional credit scores and ResidentScore are calculated.

Pro Tip:

Even with the most responsible tenants, unexpected things can happen. This is why it may be a good idea to consider requiring renter’s insurance as a stipulation for leasing.

Purpose and Calculation of Traditional Credit Scores

What is a traditional credit score? Put simply, a traditional credit score is a numeric representation used to help predict the likelihood of repayment.

Traditional credit scores are usually designed to rate a consumer’s ability to repay debt. They are often used for things like:

- Home loans

- Personal or business loans

- Car loans

At the most basic level, lenders use credit scores in an effort to help understand if there are any potential risks to lending to a specific person.

How Traditional Credit Scores are Calculated

Different companies might calculate a credit score in slightly different ways. According to TransUnion, in general, credit scores are calculated based on a person’s:

- Payment history: 40%

- Credit usage: 34%

- Credit depth (the number and age of accounts): 21%

- Recent credit: 5%

On top of that, things that might negatively impact someone’s credit score include:

- Payments that are 30, 60, or 90 days late

- Accounts that have gone to collections

- The length of credit history

- Types of credit

- New credit applications

How Landlords Use Credit Scores and Other Reports

In general, a credit score can help lenders predict what to expect from a borrower. So, it makes sense that landlords would look at a person’s credit background as part of their rental decision process .

However, as a landlord or property manager you should consider using a variety of information about your prospective tenant to help you make that decision. Tenant screening should include financial scrutiny, but also other data, such as:

- Credit Report: take a look into your potential rental applicant’s financial history to help recognize any worrying habits or potential red flags.

- Criminal background check: SmartMove searches millions of criminal records to look for a potential match to your applicant. This can help you determine if there are any past crimes .

- Eviction history: This report may help detect previous eviction-related proceedings connected with your prospective tenant.

- Income Insights: May help confirm your potential applicant makes the salary they claim on the rental application.

Then, on top of these reports, included in every SmartMove screening package is ResidentScore. Just as auto insurance risk models attempt to help predict the likelihood of an insurance claim and mortgage risk models are designed to help predict the likelihood of foreclosure, ResidentScore was designed specifically for landlords to help predict eviction risk.

This is why ResidentScore works for tenant screening.

Below, you’ll find more details about ResidentScore and how it works.

SmartMove ResidentScore: What It Is & How It Works

Like a traditional credit score, a ResidentScore is a three-digit number that may help you analyze someone’s history. Although the two numbers look similar, they are actually different.

Unlike traditional credit scores, ResidentScore was specifically designed to help predict the potential outcome of a lease. It is a proprietary calculation that was developed by analyzing millions of residents and the extensive records of TransUnion––a major credit agency with forty years of data expertise.

Similarities of a Traditional Credit Score and ResidentScore

- Both calculations result in a three-digit number

- Both range from 350 to 850

- Both have 850 as the best possible score

- Both analyze a person’s past habits

Differences Between a Traditional Credit Score and ResidentScore

- A traditional credit score was built primarily for loans and money lending

- A ResidentScore was designed specifically for the rental market

If, like many landlords, you want to help protect rental income, it can be considered good practice to screen your prospective tenant––and with the right tools to help reduce potentially catastrophic outcomes.

Pro Tip:

It’s crucial to use reputable providers and background check methods when vetting potential tenants. If you aren’t careful, risky screening practices may decimate your property business.

ResidentScore is tailored to the unique needs of landlords and built to help predict eviction risk better than a traditional credit score. As stated, not all credit scores are the same.

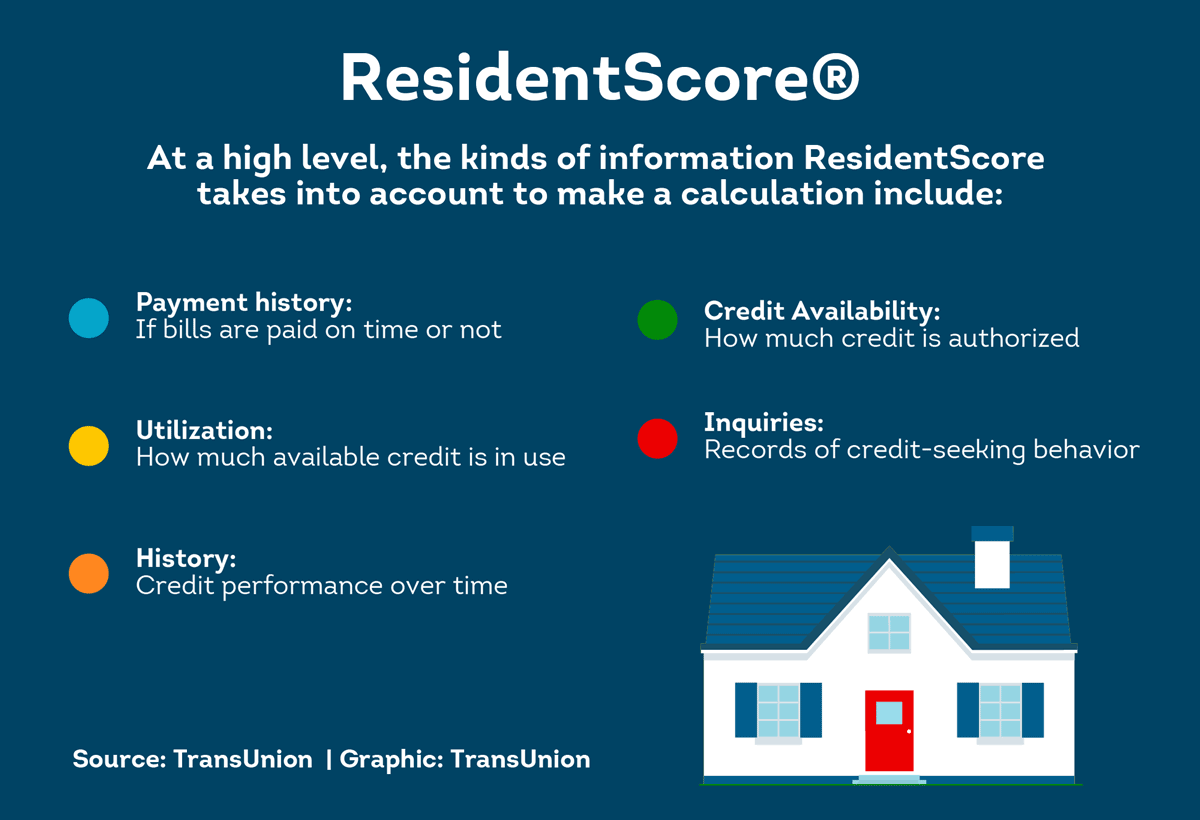

At a high-level, the kinds of credit information ResidentScore may use to include:

- Payment history: If they pay their bills on time or not

- Utilization: How much available credit they use

- History: Their credit performance over time

- Credit Availability: How much credit they have

- Inquiries: Their credit-seeking behavior

What ResidentScore Looks Like and What Numbers Mean

To help make it easier to understand, ResidentScore uses a familiar scoring range of 350-850, which is a common range in traditional credit scores.

- 350 is the lowest score possible

- 850 is the highest score possible

These low and high numbers are the same as a traditional credit score.

What’s a Good ResidentScore for Renting?

ResidentScore is designed to assess the level of potential eviction risk a tenant may bring. This is because it was developed by analyzing millions of residents and rental outcomes.

Statistically, different ranges of a ResidentScore may bring with it a correlated level of future eviction risk, according to SmartMove research.

While there may not be definitive “good” or “bad” ResidentScore, different score ranges may carry with them different potential risks. And, knowing about these scores and potential risks ahead of time may help you make more informed rental decisions. Even so, do remember that every situation is different.

People change and there are plenty of legitimate reasons why someone might have a lower ResidentScore. For example, they might have had a hard time due to circumstances outside of their control, but are now rebuilding their life and history.

This is why it’s so important to look at every potential tenant as an individual and get to know them through many types of screening.

Pro Tip:

If you do all the work of finding great tenants, you may not be eager to see them go after only a year. Read what you should know about renewing a lease with existing tenants.

This article covers the following topics:

How Landlords Can Benefit from SmartMove Reports like ResidentScore

The bottom line is: you can use a traditional credit score to evaluate your tenant’s financial behavior. However ResidentScore may be a better match for predicting rental outcomes. After all, rental screening is the intended marketplace.

In addition to ResidentScore, SmartMove offers several tenant screening reports that may help you get a look at a potential applicant’s background. These include:

- Credit Report: Does your rental applicant have a habit of paying bills on time or a ton of debt? Check out the details of their financial history.

- Criminal Background Check: Scouring hundreds of millions of criminal records looking for a potential match to your applicant.

- Previous Eviction Report: Does your potential tenant have a history of rental non-payment? This report may help find eviction-related proceedings potentially connected to your hopeful tenant.

- Income Insights: For many landlords, dealing with tenant payment problems is one of the most significant stressors of the job. Income Insights can help you confirm your prospective tenant actually makes what they claim on their application.

- Identity Check: Finally, this important report may help you confirm that your rental applicant is actually who they say they are.

Trusted by over 600,000 landlords and over 4.4 million tenants, SmartMove reports are backed by TransUnion––a major credit agency with four decades of data expertise. Getting information may help you identify a quality tenant faster.

The fully online process returns results quickly. Most reports are delivered the same day after the applicant verifies their identity. Plus, there are no sign-up costs, subscriptions, minimums or hidden fees. Simply sign up and start screening immediately.

More specialized tools may save you time and effort. Find better ways to get the job done with fast, flexible tenant screening through SmartMove.

SmartMove

Great Reports. Great Convenience. Great Insights.

ResidentScore FAQs

When it comes to assessing someone’s credit history vs. income for a rental, both may be important––and serve slightly different purposes.

- Credit history can help you verify that your rental applicant has a history of paying debts on time and has good financial habits overall.

- Income verification helps you confirm that your potential tenant has money coming in and may be able to afford the rent.

Both of these may be helpful pieces of information when deciding who to rent to. Then, when you also get a ResidentScore, you may get a robust financial picture of your applicant and their potential risks.

It depends––on the person and the reason for their low score. Both traditional credit scores and ResidentScore are used to help predict outcomes. Generally, the lower the score, the more risk. This means, someone with a low score is likely to potentially be higher risk.

Ultimately, as you review the applicant’s background history, it’s up to you to decide if your tenant’s financial situation is acceptable or not.

Know your applicant.

Additional Disclosure:

For complete details of any product mentioned in this article, visit www.transunion.com. This site is governed by the TransUnion Rental Screening Privacy Policy Privacy Notice located at TransUnion Rental Screening Solutions, Inc. Privacy Notice | TransUnion.